SCStock

SCStock

Runway Growth Finance Corp. (NASDAQ:RWAY) is a business development company (“BDC”) that was formed in 2015 but has only been public since October 2021. This BDC and its baby bonds fly under the radar, which is where we often find the best values; and this one is no exception. In fact, there has not been a single article on RWAY before on Seeking Alpha.

RWAY provides loans to growth companies and late-stage companies, and the vast majority of these loans are senior secured loans; basically, the safest types of loans that BDCs issue. They currently have only 1 non-performing loan in their portfolio.

While BDCs are allowed to take on leverage of 2 to 1 (liabilities twice NAV), as of RWAY’s latest quarter, their liabilities were only .6 to 1. This is extremely low leverage, as most BDCs have leverage of at least 1 to 1.

Since their latest quarter, they issued $45 million of a new bond, symbol RWAYZ. With the money raised from the sale of RWAYZ, RWAY intends to pay down their credit facility. So, leverage should remain unchanged, at least initially. However, they do plan to do some reborrowing from the credit facility pay down for corporate purposes. But even if they use all $45 million raised from this bond offering for corporate purposes, their leverage will only rise to .7 to 1, still way below the 2 to 1 limit and still one of the least leveraged BDCs out there.

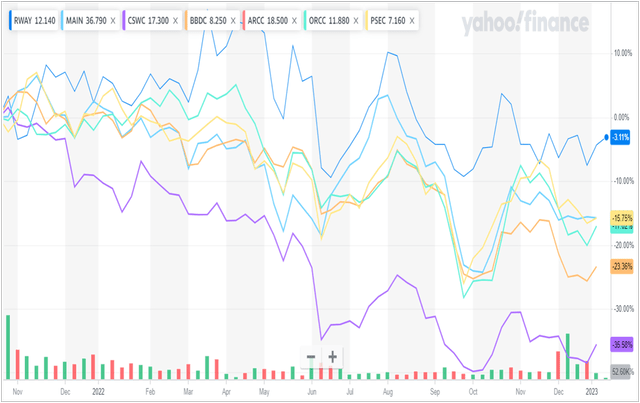

Since its inception, RWAY has handily beat the well-known BDCs like (MAIN), (ARCC), (CSWC), etc.

Yahoo Finance

Yahoo Finance

During this miserable bear market, RWAY is only down 3% while other BDCs are down large double-digits in percentage terms, with some down more than 20% and even 30%.

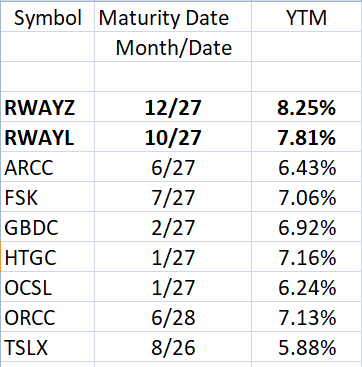

Runway Growth Finance Corp. has 2 baby bonds. Symbol (NASDAQ:RWAYZ) last traded at$25.06. It matures on 12/31/2027 with a current 8.25% yield-to-maturity (YTM). The other is symbol (RWAYL), which last traded at $24.95. It matures on 7/28/27 and has a YTM of 7.85%.

While RWAY’s leverage may rise to 40% if it uses all of the money recently raised for the purchase of assets rather than debt paydown, all of the other BDCs in the following chart are more highly leveraged at over 50%. And other BDCs may own a fair amount of debt that isn’t senior secured debt and thus maybe riskier debt than RWAY holds. Yet, despite RWAY’s apparent greater safety, RWAYZ and RWAYL have much higher yields than other BDC bonds. So, we have a big mispricing here that shows that RWAYZ and RWAYL are very undervalued.

The following chart shows a number of other BDC traditional bonds and their yields-to-maturity (YTM). The bonds that were selected from these companies are those that have maturity dates that are closest to the RWAY baby bonds.

Author

Author

It doesn’t take but a very quick look to see huge value in the RWAY baby bonds, especially RWAYZ.

And for those who own the low-quality BDC baby bond (GECCO), its YTM is only 6.7% and should definitely be sold in favor of purchasing RWAYZ. HXCY is another must swap baby bond. Its YTM is only 6.38% and it doesn’t mature until 2033. Swapping to RWAYZ is a no-brainer.

The preferred stocks that I am comparing to RWAYZ in the above chart are all investment grade, so RWAY must certainly should also be considered investment grade, although it has not been rated. But it doesn’t much matter, as no BDC bond has ever gone bad. In fact, no BDC preferred stock has ever gone bad. The legal requirement for BDCs to keep leverage below 67% has always kept them out of trouble, including even the BDCs with the worst managements who destroyed common shareholder value.

At its current price of $25.06, RWAYZ is the better value versus RWAYL, but RWAYL is probably the second-best BDC baby bond out there. RWAYZ may be benefitting from being new, with the likelihood that underwriters are still selling shares to the public. And also, it is likely that this baby bond is just unknown as no Seeking Alpha authors have written even one article on RWAY – until now.

From my observation of the trade book, it seems that there are some large sell orders which are likely from underwriters, as there is no reason for the public to be selling. All public owners of this stock made their purchases very recently, so it is doubtful they would be dumping shares so quickly in what has been a very strong preferred stock market of late.

Thus, this looks like a great entry point for this very undervalued baby bond RWAYZ, and I would expect it to have a nice rally once the underwriters are done selling. In doing a fairly exhaustive search of BDC bonds, RWAYZ stands out as a real bargain and has yet to rally with market. It has some catching up to do.

Those who follow fixed income will know that an 8.25% YTM on an ostensibly investment grade bond is outstanding; especially one that is relatively short term.

Are you looking to start building a Fixed Income Portfolio?

Conservative Income Portfolio targets the best Preferred Stocks and bonds with the highest margins of safety. We strongly believe that the next decade will belong to fixed income irrespective of whether you are conservative or aggressive in your approach! Get in on the ground floor of our recently started Bond and Preferred Stock Portfolios.

If undervalued fixed income securities, bond ladder, “pinned to par” investments and high yielding cash parking opportunities sound like music to your ears, check us out!

Psst! You get access to our options portfolio as a bonus!

This article was written by

Trading preferred stocks and fixed income securities for more than 25 years and stocks in general for 35 years. Author of many Seeking Alpha articles and Editor’s Picks articles.

Disclosure: I/we have a beneficial long position in the shares of RWAYZ AND RWAYL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.